Relocating for work or full-time education brings a wave of logistical challenges, but it also opens the door to significant tax relief through the Canada Revenue Agency (CRA). When you move at least 40 kilometres closer to your new workplace or school, you can claim eligible moving expenses to reduce your taxable income. However, complications arise if the CRA reviews your tax return and reduces or denies these moving expenses, which subsequently impacts your Canada Child Benefit (CCB) calculation. Because the CCB is a non-taxable monthly payment based directly on your Adjusted Family Net Income (AFNI), any disallowed deduction artificially inflates your income and slashes your monthly benefit payments. Fortunately, you can correct this financial setback by mounting a formal dispute that ties your moving expenses directly back to your child benefit entitlements.

Step 1: Gather and Audit Your Form T1-M Documentation

Before initiating any dispute paperwork, you must meticulously review the original Form T1-M that you submitted with your tax return. The CRA frequently disallows moving expense claims due to a lack of receipts or standard logistical mismatches, such as claiming the simplified method for vehicle expenses without maintaining a proper mileage log. Collect every single receipt for real estate commissions, legal fees for purchasing your new home, temporary living expenses up to a maximum of 15 days, and utility hook-up fees. Ensure that your employer has issued a T4 slip or a formal letter confirming your start date at the new location, as this proves the move was legally valid for work purposes. Organizing these documents into a clear, chronological index will form the foundational evidence package for your dispute.

Also Read: The Complete Guide to the Canada Child Benefit (CCB) 2026

Step 2: Formally Request an Adjustment via My Account or Form T1-ADJ

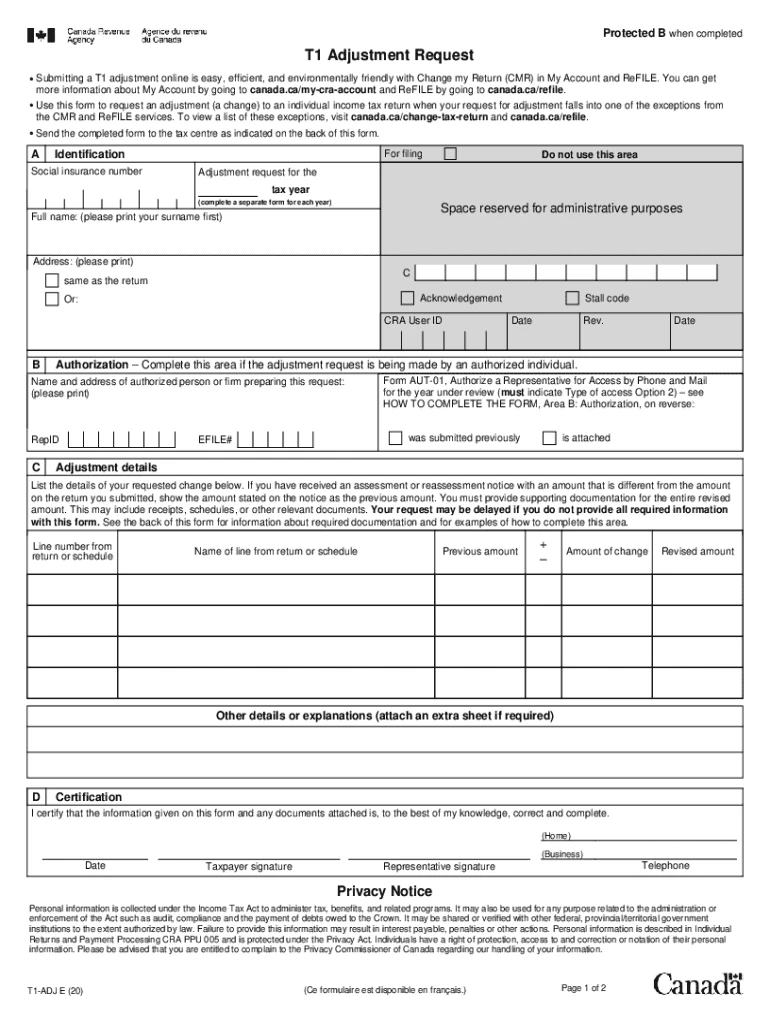

To trigger a recalculation of both your moving expenses and your resulting CCB payments, you must formally dispute the CRA’s initial assessment of your tax year. The fastest and most efficient way to achieve this is by logging into your CRA My Account portal and navigating to the “Change My Return” section to update your line-by-line moving expense figures. If you prefer the traditional paper route, you must fill out Form T1-ADJ, which is the official Adjustment Request form. On this form, you will explicitly state that you are correcting Line 21900 to include your full moving expenses as calculated on your attached Form T1-M. In the explanation section of the T1-ADJ, you must state that this deduction directly lowers your net income, which requires an automatic recalculation of your CCB entitlement under the Income Tax Act.

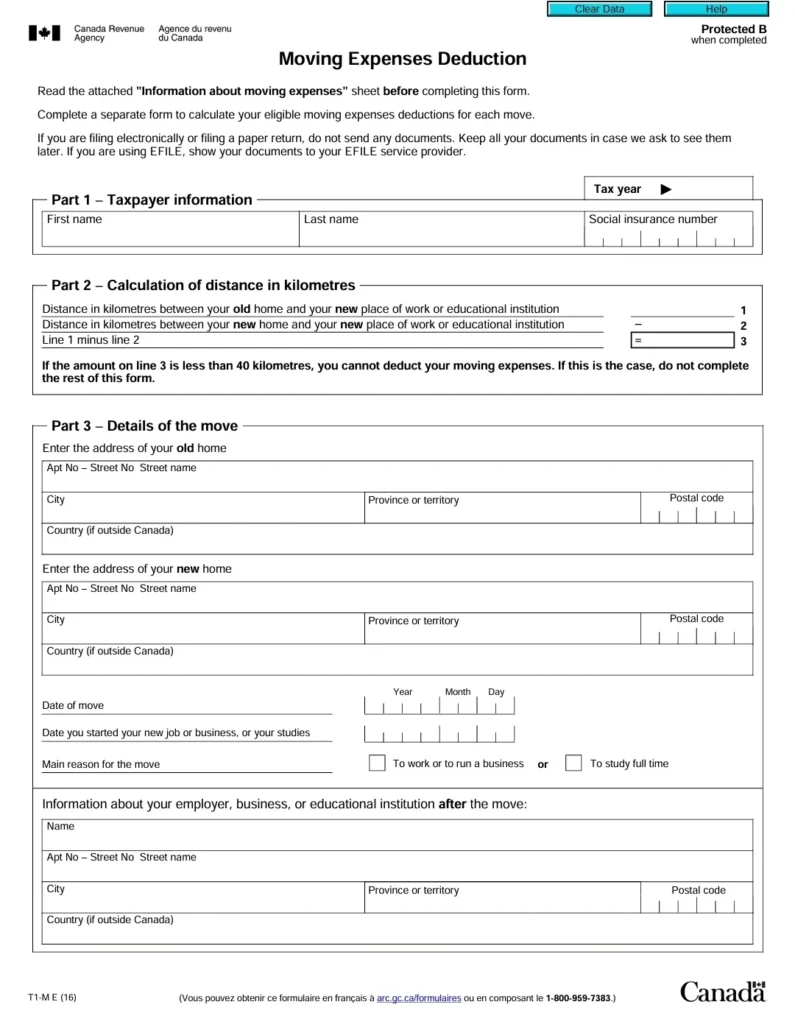

Step 3: Complete and Attach Form T1-M with Supporting Schedules

You cannot simply ask for an adjustment without providing the fully calculated Form T1-M to the agents handling your file. Download the specific version of Form T1-M for the tax year in question and carefully fill out the details regarding your old residence, your new residence, and the exact distance between them. Itemize your transportation and storage costs, travel expenses, and any costs associated with maintaining a vacant former residence up to the allowable limit. Ensure that the total amount claimed does not exceed the net income you earned at your new work location during that specific tax year, as any excess moving expenses must be carried forward to the following year instead. Attach this fully prepared form directly to your online submission or include it in your physical mail package.

Also Read: What Time of Day Does the Canada Child Benefit Drop Into Your Bank Account?

Step 4: Submit Your Official CCB Dispute and Monitor the Assessment

Once your Form T1-ADJ, Form T1-M, and all supporting receipts are ready, submit them through the “Submit Documents” feature in your CRA My Account to ensure instant digital tracking. If the CRA has already issued a formal Notice of Assessment that you completely disagree with, you may also choose to file Form T400A, which is the official Notice of Objection, within 90 days of the mailing date. Filing an objection locks in your dispute status and routes your file to an independent appeals officer rather than a standard processing clerk. Keep a close eye on your online portal for a Notice of Reassessment, which will first confirm the adjustment to your moving expenses and subsequently trigger a separate CCB notice outlining your retroactive monthly benefit top-ups.

Frequently Asked Questions

Can moving expenses affect my Canada Child Benefit (CCB) payments?

Yes, claiming eligible moving expenses directly impacts your Canada Child Benefit payments because the CRA calculates your monthly CCB amount based on your Adjusted Family Net Income (AFNI). When you successfully claim moving expenses on Form T1-M, you lower your net income on Line 21900 of your tax return. A lower net income automatically qualifies your family for higher monthly child benefit payments. Conversely, if the CRA reviews your tax return and denies your moving expenses, your net income artificially rises, which can significantly reduce your monthly CCB payments or trigger a demand to repay benefits you already received.

How do I dispute a denied Form T1-M moving expense claim with the CRA?

To dispute a denied moving expense claim, you must submit a formal adjustment request or a standard notice of objection to the Canada Revenue Agency. If you agree that you made an error or missed submitting receipts, log into your CRA My Account and use the “Change My Return” feature to upload a corrected Form T1-M along with your supporting documents. If you firmly disagree with the CRA’s assessment and have all the required paperwork, you should submit Form T1-ADJ by mail or file an official Notice of Objection within 90 days of the date on your Notice of Assessment to have an independent appeals officer review your file.

What documents do I need to prove my moving expenses to the CRA?

To win a CCB or tax dispute regarding moving expenses, you must provide a comprehensive package of receipts, distance calculations, and employment validation. The CRA requires physical receipts or detailed utility invoices for your old and new residences to prove the move was at least 40 kilometres closer to your new work or school. You must also supply explicit documentation such as moving truck rental agreements, real estate commission statements, legal fees for home purchases, and temporary living receipts up to 15 days. Finally, provide a T4 slip, employment contract, or a signed letter from your employer confirming your official start date at the new location.

How long does the CRA take to process a CCB dispute for moving expenses?

The processing time for a moving expense adjustment or CCB dispute typically ranges from eight weeks to six months, depending on the submission method and file complexity. Online submissions sent through the “Submit Documents” feature in CRA My Account are generally processed much faster, often within eight to twelve weeks. Paper adjustments sent via Form T1-ADJ or formal Notices of Objection routed to the Appeals Division can take up to six months or longer to resolve. If your dispute is approved, the CRA will issue a new Notice of Reassessment and dynamically calculate your retroactive CCB payments within a few weeks of the tax adjustment.